International Financial Reporting Standards are a set of international accounting standards stating how particular types of transactions and other events should be reported in financial statements. IFRS are issued by the International Accounting Standards Board. International Financial Reporting Standards are sometimes confused with International Accounting Standards (IAS), which are older standards that IFRS replaced (IAS were issued from 1973 to 2000).

The goal with IFRS is to make international comparisons as easy as possible. This is difficult because, to a large extent, each country has its own set of rules. For example, US GAAP is different from Canadian GAAP. Synchronizing accounting standards across the globe is an ongoing process in the international accounting community.

The Indian government on February 21, 2011, postponed the convergence of Indian accounting standards with the international standards. The governments wanted to converged with the International Financial Reporting Standards (IFRS) from April 2011 in a phased manner. However, corporate had been lobbying to defer the implementation, arguing that they were not prepared for such a convergence right now.

|

| IFRS Proposed Roadmap for India |

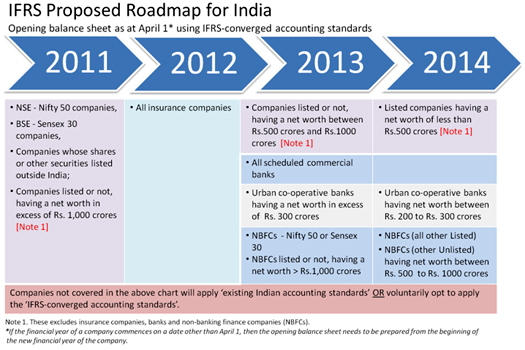

As per road map laid out by MCA earlier, companies will have to prepare their accounts as per the new form in a phased manner, beginning with companies that have net-worth of above Rs 1000 crore from April 1, 2011. While scheduled commercial banks and urban cooperative banks will adopt IFRS from April 1, 2013, all insurance conpanies convert their opening balance sheets with IFRS from April 2012. Large, listed non-banking finance companies (NBFCs), will converge their opening books of accounts with IFRS norms from April 1, 2013.

Must Read:

{kind=link}