The Indian economy has been premised on the concept of planning. This has been carried through the Five-Year Plans, developed, executed, and monitored by the Planning Commission. With the Prime Minister as the ex-officio Chairman, the commission has a nominated Deputy Chairman, who holds the rank of a Cabinet Minister. Montek Singh Ahluwalia is currently the Deputy Chairman of the Commission.

The Eleventh Plan completed its term in March 2012 and the Twelfth Plan is currently underway. Prior to the Fourth Plan, the allocation of state resources was based on schematic patterns rather than a transparent and objective mechanism, which led to the adoption of the Gadgil formula in 1969. Revised versions of the formula have been used since then to determine the allocation of central assistance for state plans.

India launched its First FYP in 1951, immediately after independence under the socialist influence of first Prime Minister Jawaharlal Nehru.

The First Five-Year Plan was one of the most important because it had a great role in the launching of Indian development after the Independence. Thus, it strongly supported agriculture production and it also launched the industrialization of the country. It built a particular system of mixed economy, with a great role for the public sector, as well as a growing private sector.

Must Read: India’s Five Year Plans at a Glance

First Plan (1951-1956)

The first Indian Prime Minister, Pandit Jawaharlal Nehru presented the First Five-Year Plan to the Parliament of India and needed urgent attention. The First Five-year Plan was launched in 1951 which mainly focused for the development of the agricultural sector. The First Five-Year Plan was based on the Harrod–Domar model.

Second Plan (1956-1961)

The Second Plan, particularly in the development of the public sector. The plan followed the Mahalanobis model, an economic development model developed by the Indian statistician Prasanta Chandra Mahalanobis in 1953. The plan attempted to determine the optimal allocation of investment between productive sectors in order to maximise long-run economic growth.

Third Plan (1961–1966)

The Third Five-year Plan stressed agriculture and improvement in the production of wheat, but the brief Sino-Indian War of 1962 exposed weaknesses in the economy and shifted the focus towards the defence industry and the Indian Army. In 1965–1966, India fought a War with Pakistan. There was also a severe drought in 1965. The war led to inflation and the priority was shifted to price stabilisation.

Don’t Miss: GDP Growth During Five Years Plans

Fourth Plan (1969–1974)

The Indira Gandhi government nationalised 14 major Indian banks and the Green Revolution in India advanced agriculture. In addition, the situation in East Pakistan (now Bangladesh) was becoming dire as the Indo-Pakistan War of 1971 and Bangladesh Liberation War took funds earmarked for industrial development. India also performed the Smiling Buddha underground nuclear test in 1974, partially in response to the United States deployment of the Seventh Fleet in the Bay of Bengal.

Fifth Plan (1974–1979)

The Fifth Five-Year Plan laid stress on employment, poverty alleviation (Garibi Hatao), and justice. The plan also focused on self-reliance in agricultural production and defence. In 1978, the newly elected Morarji Desai government rejected the plan. The Electricity Supply Act was amended in 1975, which enabled the central government to enter into power generation and transmission.

Rolling Plan (1978–1980)

The Janata Party government rejected the Fifth Five-Year Plan and introduced a new Sixth Five-Year Plan (1978-1983). This plan was again rejected by the Indian National Congress government in 1980 and a new Sixth Plan was made.

Sixth Plan (1980–1985)

The Sixth Five-Year Plan marked the beginning of economic liberalisation. Price controls were eliminated and ration shops were closed. This led to an increase in food prices and an increase in the cost of living. This was the end of Nehruvian socialism.

Seventh Plan (1985–1990)

The Seventh Five-Year Plan marked the comeback of the Congress Party to power. The plan laid stress on improving the productivity level of industries by the upgrading of technology.

Eighth Plan (1992–1997)

1989–91 was a period of economic instability in India and hence no five-year plan was implemented. Between 1990 and 1992, there were only Annual Plans. In 1991, India faced a crisis in foreign exchange (forex) reserves, left with reserves of only about US$1 billion.

Ninth Plan (1997-2002)

The Ninth Five-Year Plan came after 50 years of Indian Independence. Atal Bihari Vajpayee was the Prime Minister of India during the Ninth Five-Year Plan. The Ninth Five-Year Plan tried primarily to use the latent and unexplored economic potential of the country to promote economic and social growth.

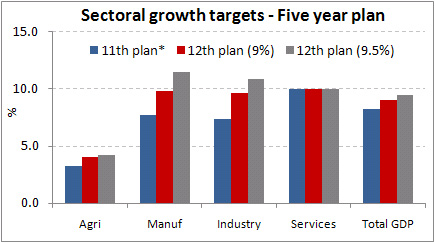

Twelfth Plan (2012–2017)

The Twelfth Five-Year Plan of the Government of India has decided for the growth rate at 8.2% but the National Development Council (NDC) on 27 Dec 2012 approved 8% growth rate for 12th five-year plan.

Read Also:

India to reduce emissions intensity of its GDP by 33-35 percent by 2030